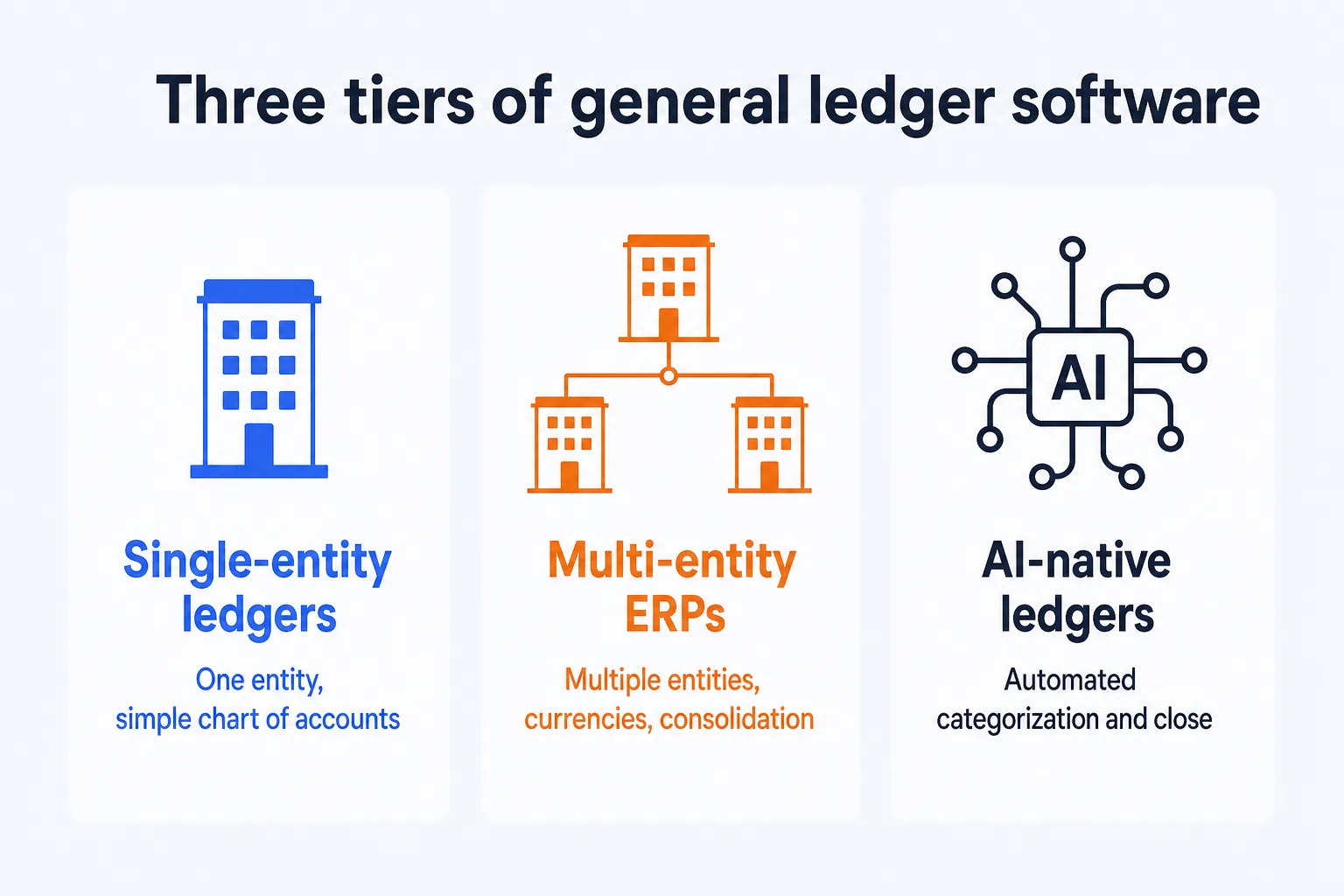

A general ledger is not the same purchase for every client, even though most software vendors describe their product the same way regardless of who is buying it. For a firm keeping books for one sole trader, "general ledger software" means QuickBooks or Xero. For the same firm's largest client, a 40-person company with three subsidiaries and a subscription revenue model, it means something closer to Sage Intacct or NetSuite. The feature list on both vendors' homepages looks similar. What actually decides the fit is entity count, how revenue gets recognized, and how complex the chart of accounts has to be, not which tool has the longer marketing page.

This list is organized around that split, plus the three questions that tell you which side of it a client sits on. For the workflow side of the wider AI bookkeeping stack, categorization, reconciliation, and the client-chasing work that surrounds the ledger, the hub guide, Best AI bookkeeping software in 2026, covers the picks by pricing structure. This article narrows in on the ledger itself: the system of record a client's books run on, and the point where a firm needs to move a client off a small-business ledger and onto something built for consolidation.

What a general ledger actually is, and how it differs from a journal

A journal is the chronological record. Every transaction gets an entry, in the order it happened: an invoice raised, a bill paid, a bank fee charged. A general ledger is what those entries roll up into. It holds one account for cash, one for accounts receivable, one for each expense category, and each account carries a running balance built from every journal entry that touched it. The journal answers "what happened and when." The ledger answers "what is the balance right now." Software described as a "ledger system" or "GL system" does both jobs at once: it captures the journal entries, often automatically from a bank feed or an invoice, posts them straight into the ledger accounts, and produces the trial balance and financial statements from there.

That distinction matters for one practical reason: every credible accounting product already handles it. Asking whether a tool "has a general ledger" gets you nowhere, because they all do. The real questions are what the ledger can consolidate, whether it holds more than one entity's books without an export to a spreadsheet, and whether it can defer and recognize revenue on a schedule instead of booking it the day cash lands. Those capabilities are what split the market, not the ledger function itself.

The question that actually decides the right tier

Three questions about a client, answered honestly, narrow the shortlist before you look at a single feature page.

Does the client operate more than one legal entity, more than one currency, or need consolidated reporting across related companies? A holding structure, a group with a UK parent and a US subsidiary, or a founder running three LLCs all answer yes.

Is revenue recognized on a schedule rather than at the point of sale? A SaaS company billing annually but recognizing monthly, a services firm recognizing revenue over a contract term, or a business with deferred obligations needs a ledger that can automate that schedule rather than track it in a spreadsheet next to the books.

Does the chart of accounts need to split by dimension, department, location, project, or class, rather than staying flat? A single-location retailer does not. A company reporting profitability by region or by product line does.

A single-entity, cash-in cash-out business with a simple chart of accounts never needs to graduate, no matter how large its revenue gets. What forces the move is entity count, recognition complexity, or dimensional reporting, not size on its own. Keep that in mind before recommending an ERP-grade system to a client who only needs a cleaner QuickBooks file.

Best general ledger software for single-entity clients

Most clients answer no to all three questions above, which is why these ledgers cover the majority of a typical firm's book.

QuickBooks Online, starting around $38 a month, is the default in the US for good reason: bank feeds, invoicing, and financial statements in one place, with the largest small-business app ecosystem and an AI layer, Intuit Assist, included at no extra cost for categorization and receipt capture. Xero, from about $25 a month, does the same core job with a cleaner interface and the stronger footprint in the UK, Australia, and New Zealand. If a client's accountant already works in Xero, staying there usually beats migrating for a marginal feature difference.

Zoho Books fits a micro-business watching every dollar: it stays free for companies under $50,000 in annual revenue, then adds multi-currency and inventory on paid tiers. For UK clients specifically, FreeAgent and Clear Books both handle HMRC-recognized Making Tax Digital filing for sole traders and small limited companies, which QuickBooks and Xero also do but at a different price point. Wave Accounting is the pick for a solo trader or freelancer who needs proper double-entry bookkeeping and cannot justify a subscription: it is permanently free, with double-entry rigor built in rather than a stripped-down version of it.

None of these tools consolidate multiple entities without exporting to a spreadsheet, and none defer revenue on a schedule beyond basic invoicing. That is not a weakness. It is the correct shape of software for a client who will never need either capability.